Electric cars seen as future of transport, but China holds the keys

Electric cars seen as future of transport, but China holds the keys

PRC has cornered market on vital ingredients for batteries: rare earth elements

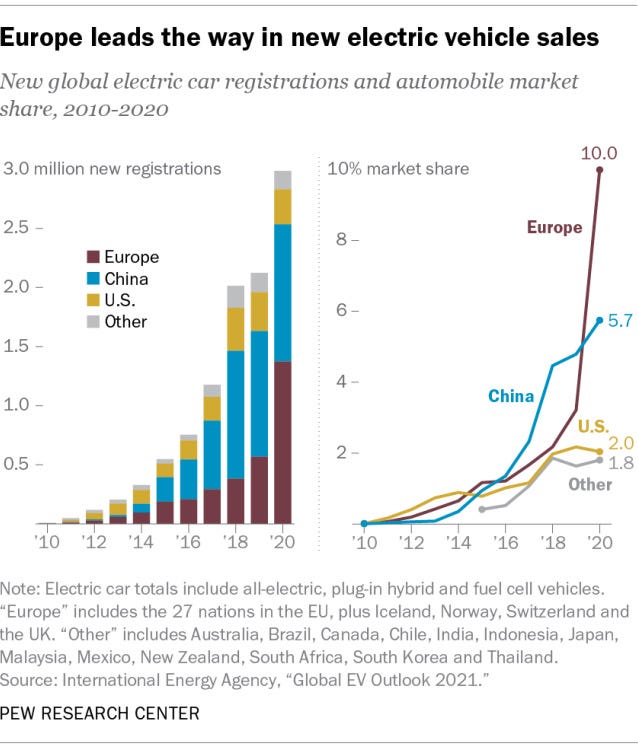

At the turn of the century, electric vehicles were mostly the stuff of science fiction. They were a little more than a gleam in the eyes of Elon Musk.

Today they are seen as the future of transportation technology. It has been a rapid and total transformation.

Even though electric vehicles account for only about 10% of all current vehicle sales, the graphs are going parabolic: sales are increasing exponentially every year.

Part of the reason is the rapid advance in battery technology. Major auto makers, including Tesla, are investing billions both in auto production facilities and battery factories.

The problem is they are a bit late to the game.

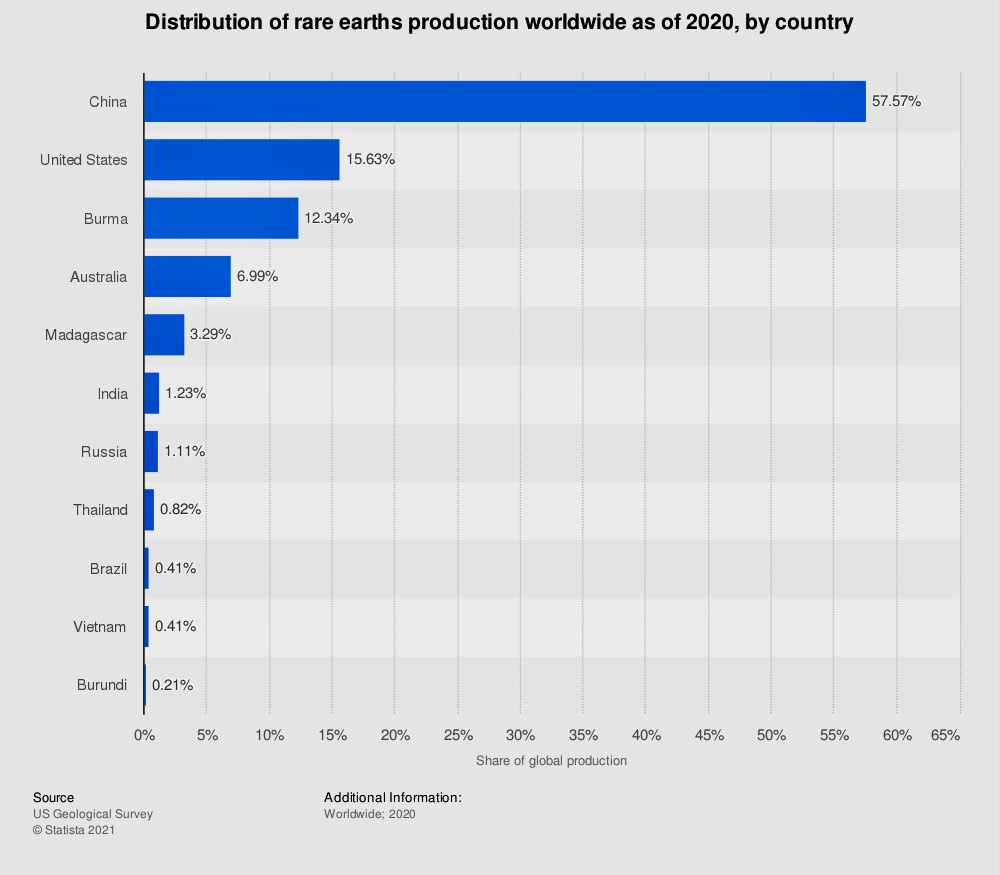

For more than three decades China has been investing massively in the crucial components that go into batteries that power all sorts of electrical appliances but especially vehicles and phones: what are known as “rare earth” elements.

Today the Peoples Republic of China has cornered the market.

It is easy to find alarming reports that demonstrate China's dominance in this field today, and – most likely – well into the future.

To understand how we got to this impasse, some background is needed.

Of the 17 chemical elements classified as “rare earths” two play an outsize role in battery manufacturing: Lithium and Cobalt.

Also, there is a big difference between mining rare earths and processing or refining them. So, Australia has the largest deposits of Lithium in the world, but must export most of what it extracts to China for processing.

For historical and structural reasons, China has become the world’s biggest processor of rare earth elements.

When it first embarked down this road, its concern for environmental degradation was minimal to non-existent.

Processing of rare earth minerals is messy, resulting in sometimes toxic by-products.

But, with China’s command economy, the government’s priorities are strictly enforced – sometimes irrespective of the costs, environmental or otherwise.

These factors at least in part lead us to where we find ourselves today: the April 16, 2020 headline at Mining (dot) com China’s stranglehold on electric car battery supply chain is not an exaggeration: “Nickel-cobalt-manganese cathode chemistries dominate global lithium ion electric vehicle battery production…

“The fact that the Democratic Republic of Congo is the source of more than two-thirds of global production and China’s control of refining is north of 80%, makes cobalt a particular headache for automakers.”

“A new report by Benchmark Mineral Intelligence (more later on this) shows just what a stranglehold China has developed on the EV battery supply chain.”

The London-based battery supply chain, megafactory tracker and market forecaster Benchmark first developed a chart for testimony to the US Senate in 2019, with Managing Director Simon Moores warning that the US is “a bystander in the battery arms race.”

North America produced zero manganese and Ukraine is home to a small operation, but it’s not capable of producing feedstock for the battery supply chain.

“Benchmark says while China only mines 6% of the globe’s manganese, it is this chemical refining step in the supply chain where China has the significant advantage, with 93% of production in 2019.”

That probably does meet the level of a “stranglehold” – it is as close to a monopoly as can be.

The testimony referred to in the 2020 article was provided to a US Senate committee on Feb. 6, 2019 and can be seen at Benchmark Minerals’ Simon Moores warns Senate US a ‘bystander’ in battery arms race.

Simon Moores, Benchmark Minerals’ Managing Director, testified on the supply chains of key battery raw materials used in energy storage to the US Senate Committee on Energy and Natural Resources

“We are in the midst of a global battery arms race, in which so far the US is a bystander,” he said. “The advent of electric vehicles and energy storage has sparked a wave of battery megafactories that are being built around the world.

“Since … only 14 months ago, we have gone from 17 lithium ion battery megafactories to 70 … that’s the equivalent of 22 million pure electric vehicles worth of battery capacity in the pipeline.”

Moores told the Senate panel that the scale and speed of this growth “is unprecedented and it will have a profound impact on the raw materials that fuel these battery plants.”

Moores explained that the explosion of construction of battery megafactories would also have a huge impact on the demand for critical battery raw materials of lithium, cobalt, nickel and graphite, which he called “unprecedented.”

“For example, in the next decade the demand for lithium [used in the battery industry] is set to go up 9-times, cobalt is set to go up 6-times, nickel is set to go up 5 times, and graphite anode is set to go up 9 times.”

Then came the truly alarming part – and the reason for his testimony:

“In the mining stage of these metals, How much of that mined supply does the US control? For nickel it’s zero, for cobalt it’s zero, for graphite it’s zero, and for lithium it’s one percent.

“For the chemical stage, where the knowhow comes in for using these minerals in batteries, how much capacity does the US control? Nickel it’s zero percent, cobalt it’s zero percent, graphite it’s zero percent, and for lithium it’s 7%.”

In the manufacturing stage, where they make the actual batteries – the consuming plants – Moores was just as bleak:

“In 2018 the US had 9% (of battery manufacturing), that was mainly from the Tesla Gigafactory in Nevada and by 2028 we’re only forecasting 10%. We’re forecasting a relative flatline as this industry grows.”

This is on its own not good news. But taken in context of what’s forecast in China, it is even worse:

“China is on track to have 65% of battery capacity by 2028,” Moores testified. “It already has 51% of lithium chemical capacity, 80% of cobalt chemical capacity, 100% per cent of graphite anode capacity and a third of nickel chemical capacity.”

Moores was talking mostly about 2018, the latest year for which he had data. One might think that after such a wake-up call, the US would have immediately embarked on a crash program to correct the situation. But, one would have been wrong.

Not much changed.

So we find out in a September, 2020 study by the Institute for Energy Research that China Dominates the Global Lithium Battery Market

“After years of planning, China now dominates the world’s production of new generation batteries that are used in electric vehicles and most portable consumer electronics such as cell phones and laptops,” the study reports.

It predicts that as the demand for electric vehicles grows, “it is expected that most of them will be built with Chinese batteries, and most of those batteries will be lithium ion … because of their high energy per unit mass relative to other electrical energy storage systems.

“For the foreseeable future, the United States will be dependent on Chinese supply chains to produce the batteries that power America’s technologies.”

In 2019, Chinese chemical companies accounted for 80 percent of the world’s total output of raw materials for advanced batteries, the report said.

“China controls the processing of pretty much all the critical minerals – rare earths, lithium, cobalt, and graphite. Of the 136 lithium-ion battery plants in the pipeline to 2029, 101 are based in China.”

This cannot by any interpretation be a good situation for the US – to be dependent on what we can kindly call a "strategic competitor" for the most essential ingredients of the post-industrial era.

It is a very short step to recognizing this as a national security issue.

Which is just what happened in this September 2021 article in National Defense Magazine China Maintains Dominance in Rare Earth Production

It begins with a relatively innocent quotation: “In 1987, then-Chinese President Deng Xiaoping famously said, ‘The Middle East has oil. China has rare earths.’ ”

Most people at the time did not fully understand it. “But China understood that rare earths were going to be the backbone of manufacturing,” said Pini Althaus, CEO of USA Rare Earth a startup with aspirations to mine and refine the 17 elements categorized as “strategic minerals.”

While what the former Chinese president said was true, that China has vast deposits of rare earth elements to mine — so do many other nations, including the United States, Canada, Australia and Japan.

After Deng’s 1987 declaration, China legitimately partnered with foreign companies that were doing the complex work of separating rare earths from the surrounding rock and refining them, then moved the production to mainland China, Althaus said.

The article continues: “Meanwhile, the U.S. government widely thought that rare earth mining and refinement was a difficult and dirty business, so it let China do it all on the cheap so it can supply U.S. manufacturers with inexpensive rare earths.”

There are two national security issues, Althaus said. “One is, if China economically weaponizes rare earths and stops sending the refined products to the US so they can’t be used in weapons systems or commercial applications.

“Or the nation may create shortages by prioritizing its own industries such as the burgeoning electric vehicle market, which uses some of the key elements to make high-performance magnets used in engines.

“We’re seeing shortages already and those shortages are projected to increase in the coming years,” he said.

Weaponizing rare earth elements

It would not be unprecedented. In 2010, China allegedly pulled the “rare earth card” in response to a territorial dispute with Japan, which led to an undeclared Chinese embargo.

These actions were challenged by the United States, the European Union, and Japan, resulting in a ruling against the country’s export quotas by the World Trade Organization (WTO).

The WTO ruled that the export quotas represented an unfair restriction that allowed China to control global rare earth prices. Because China does not impose the regulations on mining rare earths that other countries do, “toxic wastes from rare-earth facilities have poisoned water, ruined farmlands, and made people sick.”

The National Defense article noted that “China’s strategy extends to other strategic minerals such as cobalt, of which it has established a monopoly, and lithium, needed to make lithium-ion batteries also found in electric vehicles.”

We are well beyond turning back on the road to electrification of our transportation systems. The imperative of a warming world demands it.

No realistic scenario allows us to continue to burn fossil fuels at the rate required to sustain automobile and truck traffic around the globe.

It seems that without immediate concerted action the entire world could be held hostage to the whims of an increasingly assertive Chinese government. It is a geo-strategic dead end.

Future generations may come to regret the mistakes of the past 30 years. We have to live with them as best we can.

Very interesting indeed. Thanks for sharing, Warren.

Thank you Warren for an outstanding article. China's huge surplus of rare earth elements puts it in an excellent position to transform transportation itself in the coming decades. Will China do that? It's difficult to say. Profits from individual vehicles, like those that glut our freeways daily, are potentially astronomical. However, a more visionary approach would strive to develop cheap, efficient mass transit.

Thank you Warren!